The car audio industry is entering a new phase of sustained growth, fuelled by rapid changes in vehicle architecture and how drivers interact with in-car technology.

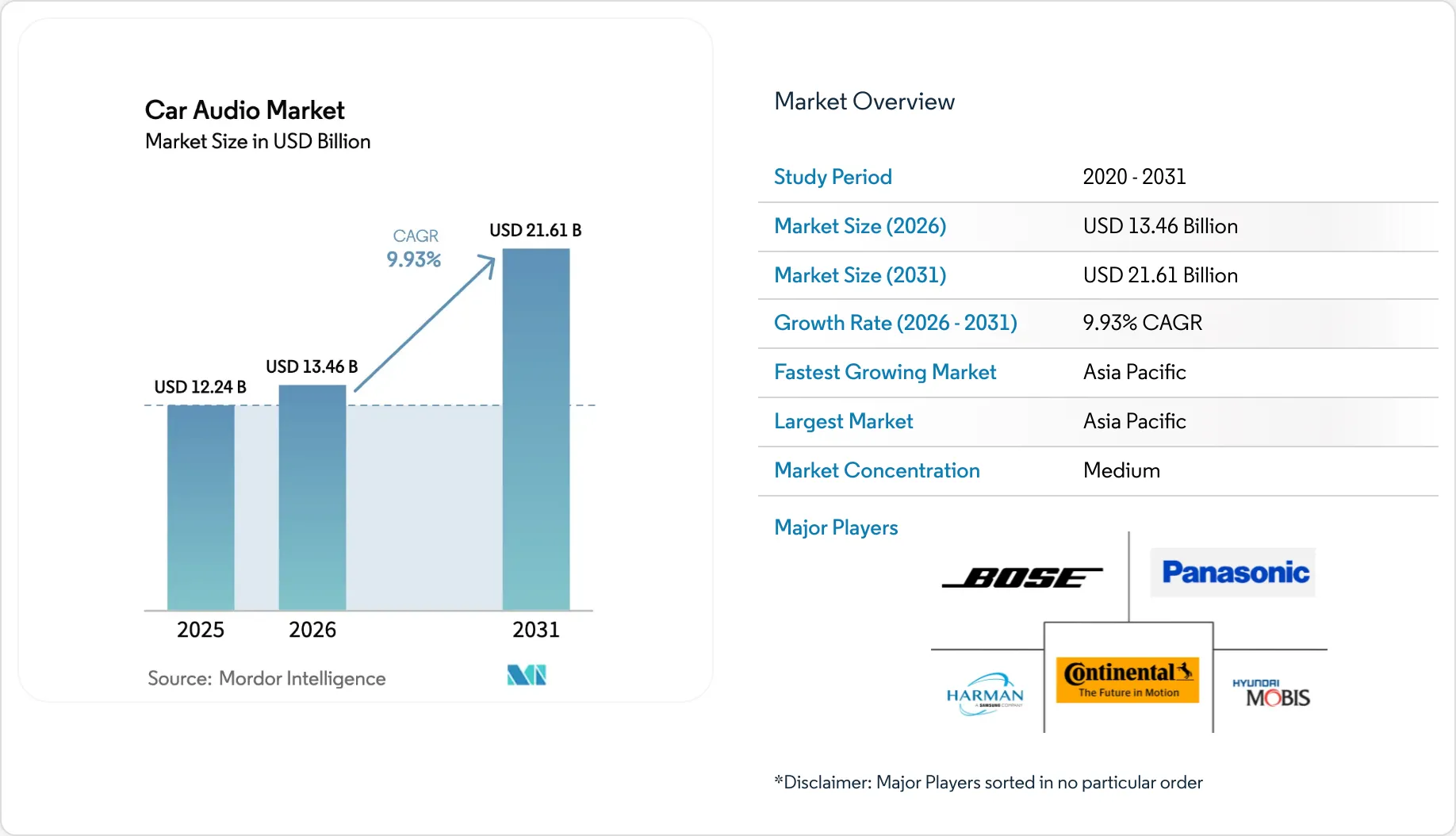

New research from Mordor Intelligence forecasts the global car audio market will grow from around US$13.46 billion (£9.95 billion approx) in 2026 to US$21.61 billion (£15.98 billion) by 2031, representing a compound annual growth rate of just under 10%.

While the numbers are strong, the more important story is what’s driving them.

Software-defined vehicles change the rules

A major shift is underway as infotainment systems evolve into software-defined platforms. Rather than fixed hardware setups, in-car audio is increasingly shaped by software updates, cloud connectivity and over-the-air feature enhancements.

This is opening the door to more advanced audio processing, smarter system calibration and deeper integration with voice and AI-driven controls – all of which extend far beyond traditional speaker-and-amplifier set-ups.

EVs reshape system design and demand

Electric vehicles are also playing a major role in reshaping system design. With efficiency now critical, manufacturers are adopting more compact, energy-efficient Class D amplification platforms that reduce heat and power loss without compromising output quality.

At the same time, the absence of engine noise is changing consumer expectations inside the cabin. Many EV owners are now actively upgrading low-frequency performance, particularly subwoofer systems, to restore perceived depth and balance to in-car audio.

Asia-Pacific leads, while North America upgrades

Regionally, Asia-Pacific remains the dominant force, accounting for more than 43% of global market share in 2025, supported by high vehicle production volumes and rapid technology adoption across China, Japan, South Korea and India.

North America, meanwhile, is increasingly defined by upgrades rather than first-time installations, with growth driven by premium factory audio packages, software enhancements and subscription-based features.

OEM dominance, aftermarket acceleration

OEM systems still dominate the market, accounting for around 68.32% of global share in 2025, reinforcing how strongly car audio remains embedded at factory level.

However, the aftermarket is growing faster, expanding at an estimated 12.18% CAGR as demand shifts toward customisation, plug-and-play upgrades and software-enabled tuning.

Much of this growth is being enabled by online ecosystems that use VIN-based configurators to match vehicles with compatible harnesses and components, significantly reducing installation complexity.

For specialist installers, this is also reshaping business models. Many are moving away from pure hardware sales toward higher-value services such as DSP tuning, firmware updates and software-based sound profile configuration – services that can evolve over the lifetime of the vehicle.

Taken together, these trends are extending revenue opportunities well beyond the point of sale, turning car audio into a long-term, software-influenced ecosystem rather than a one-time hardware purchase.

And that is ultimately why the category continues to grow – not just in size, but in complexity, capability and commercial opportunity.

Here's a quick snapshot of the main figures:

Market size

Key growth drivers

Regional breakdown

Key segments

Market structure

More details available at the website below.

© Copyright 2026 Smart Media Publishing. All Rights Reserved.